Social Security, the program you may have spent a lifetime paying into, is designed to offer stability, supplemental income, and other valuable benefits that can play a role in your overall financial strategy after you retire.

We’ve pulled together answers to 10 questions our clients ask most frequently regarding Social Security. If you are nearing retirement, this Q&A is designed to help you better understand what to expect from Social Security.

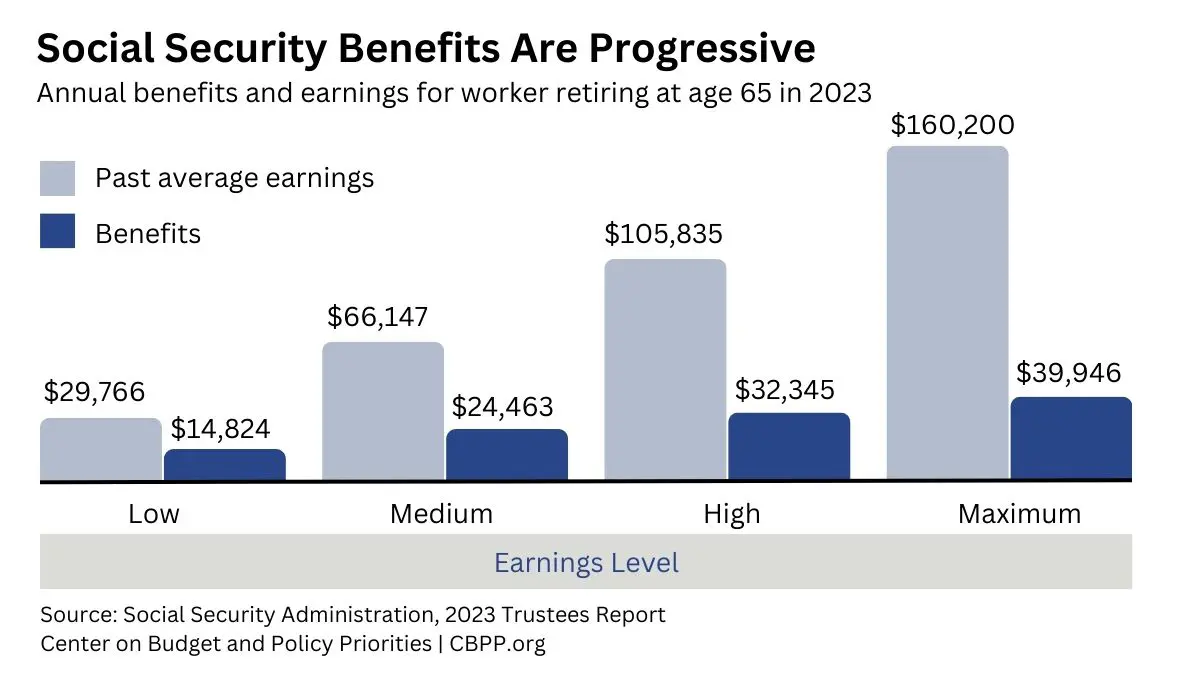

1. How are Social Security Benefits Calculated?

Social Security benefits are typically computed using “average indexed monthly earnings.” This average summarizes up to 35 years of a worker’s indexed earnings. Social Security applies a formula to this average to compute the primary insurance amount (PIA). The PIA is the basis for the benefits that are paid to an individual.

In general, the higher your earnings (up to $160,200, the maximum taxable amount in 2023), the higher your benefits.1

2. When Can I Start Collecting Social Security Benefits?

You can claim Social Security benefits as early as age 62, but the longer you delay starting, the larger your monthly payments may be.2

If you wait until full retirement age to collect Social Security retirement benefits, you can receive 100% of your monthly retirement benefits.

If you wait even longer beyond your full retirement age, the Social Security Administration increases your benefit by up to 8% for every year you wait (up to age 70).

The accompanying chart from the Social Security Administration outlines how monthly benefit amounts differ based on the age at which you decide to start receiving them.

3. Can Social Security Impact My Retirement Cash Flow?

While you may have various sources of income to tap into during retirement, Social Security should not be overlooked when preparing your distribution strategy.

Here’s a hypothetical example that outlines what it might take to replicate the income you could receive from Social Security:

- Assuming an annual benefit in 2023 of $30,000, you would need to invest approximately $1,000,000 in an investment vehicle that yields 3% to generate that same income.

Remember, this is a hypothetical example used only for illustrative purposes—it is not representative of any specific investment or combination of investments. It’s used to illustrate the cash flow potential of Social Security benefits.

4. Does My Spouse Get My Social Security On Top of Theirs When I Die?

In the event of your death, your spouse may be eligible for survivor benefits based on your Social Security record, but they will not receive these benefits in addition to their own—they’ll receive whichever benefit is higher.3

Here are some factors from the Social Security Administration website to consider about survivor benefits:

- If your surviving spouse, or a surviving divorced spouse, remarries before they reach age 60 (age 50 if they have a disability), they cannot receive benefits as a surviving spouse while they’re married.

- If your surviving spouse, or a surviving divorced spouse, remarries after they reach age 60 (age 50 if they have a disability), they will continue to qualify for benefits on your Social Security record.

- If they’re eligible for retirement benefits on their own record: If your surviving spouse, or a surviving divorced spouse, receives benefits on your record, they can switch to their own retirement benefit as early as age 62, assuming that they’re eligible for retirement benefits and their retirement rate is higher than their rate as a surviving spouse or surviving divorced spouse.

5. Is Income from Social Security Taxable?

Social Security benefits are taxable, and the rate is based on your income, which includes:4

- Adjusted gross income (includes earnings, investment income, and retirement plan withdrawals).

- Tax-exempt interest, such as interest on municipal bonds.

- Half of your Social Security benefit.

The Congressional Research Service found that the percentage of all tax returns with taxable Social Security benefits reached 33% in 2017 (the most recent data available). In 1999, fewer than 8% of all taxpayers reported taxable Social Security benefits, while the percentage is expected to increase to more than 50% by 2046.4

Here’s a summary of how the taxes on Social Security income break down. Please note that the dollar-amount thresholds have remained the same since taxes on benefits were introduced in 1984. They are not adjusted for inflation.

If you are approaching the time to start collecting benefits, there are several potential ways to manage how your benefits are taxed. The simple way is to ensure that your income is less than the threshold at which taxes apply. So, it’s critical to have a detailed understanding of your retirement accounts.

6. How Does the Cost-of-Living Adjustment Work?

Once someone starts receiving Social Security benefits, their payments may increase in accordance with the rate of inflation in the prior year.5

The cost-of-living adjustment (COLA) was 5.9% in 2021, followed by an 8.7% increase in 2022. However, three times in the past 14 years, there was no COLA increase for recipients.

7. Does Social Security Include Medicare?

Medicare and Social Security are both government programs. They aren’t the same, but they are linked. Some people become eligible for both programs at around the same time.5

Medicare provides federal health insurance for people aged 65 and older and is made up of four parts: Part A (hospital insurance), Part B (medical insurance), and Part D (prescription drug coverage). It also includes Part C, or Medicare Advantage, a bundled alternative to Original Medicare offered by private insurance companies that provides all the coverage of Parts A and B, plus some different rules, costs, and restrictions.

8. Can I Still Work and Collect Social Security Benefits?

Yes, you can collect Social Security benefits as early as age 62, even if you decide to keep working. Just be aware that your age and earnings may impact the amount of the benefits you receive during those working years.

Working won’t permanently reduce your Social Security benefits if you start taking them early. Once you reach full retirement age, your monthly benefit will increase, taking into account prior benefits detained due to earnings.6

9. When Should I Start Taking Benefits?

Deciding when to begin taking Social Security is a critical decision and one of our most common questions. It may seem straightforward, but it’s more complex than it looks.

Since everyone’s circumstances are unique, there are a few considerations that you may want to take into account:

- Will you continue working? You may see some of your payments withheld if you are still working while collecting early benefits.

- Are you married? Does your spouse anticipate benefits?

- How is your health? Your health status could affect your decision on when to start taking benefits.

10. Will Social Security Go Bankrupt?

Social Security has often been called the “third rail” of politics because of the negatives associated with tackling the issue. However, relatively modest changes could place Social Security on sounder financial footing.5

While Social Security does face some challenges, there are several potential approaches that are being considered in Washington, D.C., to reinforce the program. It’s possible that one of the approaches might be proposed in the years ahead.

It’s estimated that without Social Security, 21.7 million more people would live below the poverty line. At some point, lawmakers are expected to address the situation.7

Contact Us with Questions

As financial professionals, understanding your sources of retirement income is an integral part of our services. If you have any questions about social security, please do not hesitate to contact us. We’re here to help, and we may have resources that can help you better understand your benefits.

![]()

- CenteronBudgetandPolicyPriorities.org, April 17, 2023

- Nerdwallet.com, May 5, 2023

- SocialSecurity.gov, 2023

- GOBankingRates.com, July 29, 2023

- Nerdwallet.com, September 29, 2022

- Ameriprise.com, 2023

- CenteronBudgetandPolicyPriorities.org, March 29, 2023